Every Caribbean insurer and government agency knows the compliance burden is growing. New CBCS directives, tightening AML frameworks, and cross-border reporting requirements arrive faster each quarter.

The standard response is to add more checks. More forms. More manual reviews. More friction for customers and staff alike.

There is a better path — and the organisations that find it first will turn compliance from a cost centre into a competitive edge.

The Blanket-Check Problem

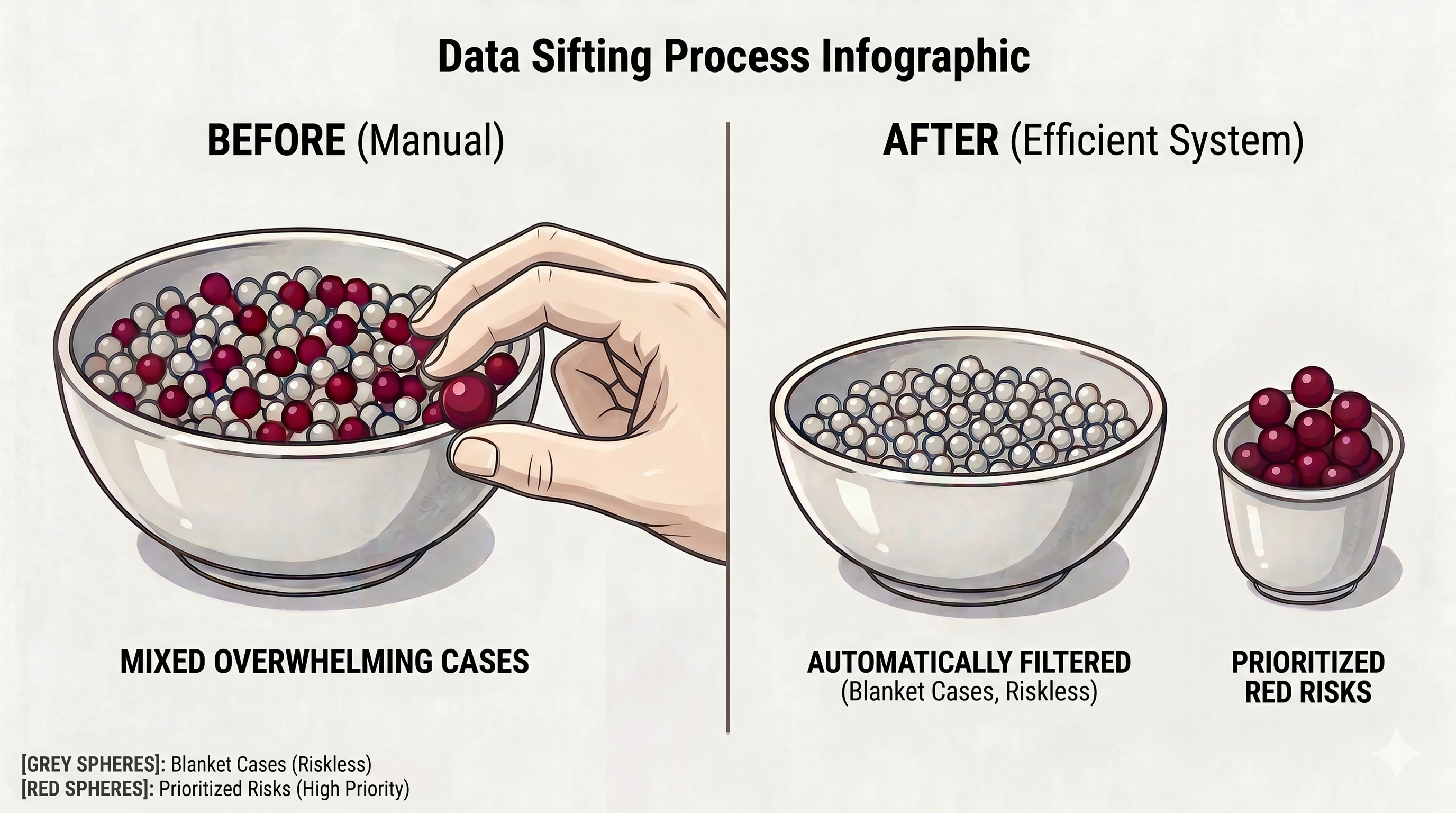

Most compliance programmes in the Caribbean apply the same level of scrutiny to every customer, every transaction, every onboarding. This feels thorough. In practice, it is the opposite.

Blanket checking means your highest-risk relationships get the same attention as your lowest-risk ones. Analysts spend hours verifying low-risk retail customers while genuinely complex cases receive the same templated review. The result: regulatory exposure increases even as compliance costs rise.

Regulators have noticed. The CBCS and international supervisory bodies increasingly expect risk-based approaches — not because they reduce effort, but because they focus effort where it actually matters.

What Risk-Based Means in Practice

A risk-based compliance framework starts with segmentation. Not all customers carry the same risk profile, and not all transactions warrant the same scrutiny.

In practice, this means:

- Tiered onboarding. Low-risk retail customers move through a streamlined KYC process. High-risk relationships — politically exposed persons, complex corporate structures, cross-border arrangements — receive enhanced due diligence from the start.

- Dynamic monitoring. Transaction monitoring rules adapt based on the customer’s risk tier and behavioural patterns, rather than applying identical thresholds across the portfolio.

- Proportionate documentation. The depth of ongoing review scales with risk. Annual reviews for low-risk segments, quarterly for high-risk, triggered reviews for material changes.

The result is not less compliance. It is more intelligent compliance — the kind that actually catches problems instead of generating paperwork.

The Caribbean Context

European and North American compliance playbooks are built for different regulatory environments, different customer bases, and different risk profiles. They do not transfer directly to the Caribbean.

Consider the specifics:

- Multi-jurisdictional complexity. A Curaçao-based insurer may serve customers across Aruba, Bonaire, Sint Maarten, and the Netherlands — each with distinct regulatory expectations.

- Correspondent banking pressure. Caribbean financial institutions face heightened scrutiny from international correspondent banks. A risk-based approach provides the documentation trail that satisfies these relationships.

- Small-market dynamics. In markets where everyone knows everyone, compliance must balance rigour with relationship preservation. Risk-based approaches let you apply light-touch processes where warranted.

Building a compliance framework that accounts for these realities — rather than importing a generic one — is both a regulatory requirement and a business advantage.

From Cost Centre to Differentiator

Organisations that implement risk-based compliance well report three consistent outcomes:

- Faster customer onboarding. Low-risk customers experience minimal friction. Time-to-serve drops, and customer satisfaction increases.

- Better regulatory relationships. Supervisors respond positively to risk-based frameworks because they demonstrate genuine understanding, not just box-ticking.

- Lower total cost. Focusing analyst time on high-risk cases reduces the volume of low-value reviews. Teams do less work overall but catch more actual issues.

The competitive advantage is real: in a market where every insurer and government agency faces the same regulatory burden, the one that manages it intelligently moves faster, serves better, and operates at lower cost.

The Customer-Central Principle

At the foundation of effective risk-based compliance is a principle that sounds obvious but is rarely implemented: keep the customer at the centre.

Compliance exists to protect customers, not to inconvenience them. When a compliance programme is designed around the customer journey — understanding who they are, what they need, and what risks are genuinely present — it produces better outcomes for everyone: the customer, the organisation, and the regulator.

This is not a technology problem first. It is a design problem. The technology follows.

Getting Started

Transitioning to risk-based compliance does not require a multi-year programme. It starts with an honest assessment of your current approach: where are you applying disproportionate effort? Where are genuine risks receiving insufficient attention? What does your regulatory environment actually require versus what you have assumed it requires?

A structured review — two hours with the right expertise — can map your current position and identify the highest-impact changes.

Book a free Compliance Health Check to benchmark your current approach.